The State of the UK Recreational Bluefin Tuna Fishery 2026

Updated: 15 July 2026

Overview

The UK recreational bluefin tuna fishery is growing — and growing fast. To understand exactly who is participating, how much they are investing, and where the sector is heading, UKTuna conducted an independent survey of anglers, vessel operators, charter skippers and marine industry professionals across the UK.

With 75 responses collected from across England, Scotland, Wales and Northern Ireland, the State of the UK Recreational Bluefin Tuna Fishery Survey 2026 provides the most detailed data-led picture of the sector assembled to date. The findings document a fishery driven by highly committed, well-equipped offshore anglers who have already made substantial financial investment — and who are ready to fish far more.

This report summarises the key findings.

Who Responded

The survey drew responses from across the recreational tuna community, reflecting the breadth of people now engaged with the fishery.

72.0% of respondents are private boat owners or operators, 64.0% identify as recreational anglers, 12.0% are charter skippers or operators, 5.3% are connected to the tackle or marine industry

Many respondents hold multiple roles — for example, a private boat owner who also fishes recreationally and charters — which reflects the nature of small-scale offshore fishing operations. The data shows this is not a single-profile community: it spans private individuals, commercial charter businesses, crew members, guides and industry participants.

Of those who had engaged with the permit process, 29 respondents had applied for a permit directly, 11 had participated through a permitted vessel, and 25 had done both. Of those who answered the question directly, results were split almost evenly: 35 had been successful at some point, and 31 had not.

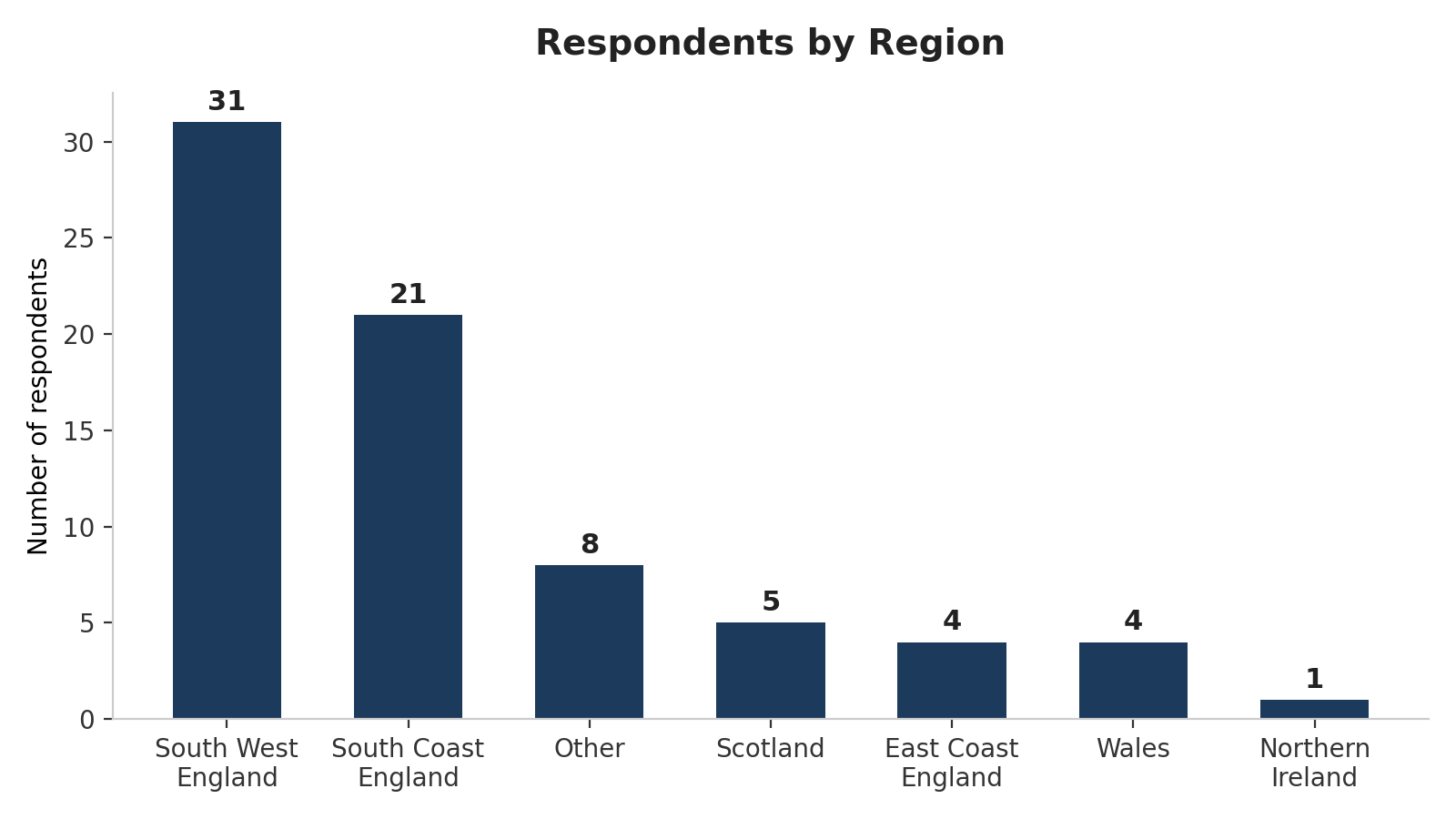

A National Fishery, Not Just a South West One

While the South West of England remains the largest single hub of UK recreational bluefin activity, the survey data makes clear this is a fishery with national reach.

More than 58.1% of respondents are based outside the South West, including active communities in Scotland, Wales, the South Coast and the East Coast. Several respondents also noted increasing tuna encounters outside traditionally recognised fishing areas, suggesting the geographic range of the UK recreational fishery may be broader than commonly understood.

Investment: A Sector Already Committed

One of the clearest findings from the survey is the scale of financial investment already made by participants — much of it before reliable long-term access to the fishery was guaranteed.

97.3% of respondents (73 out of 75) reported having already made investments connected to anticipated participation in the recreational bluefin tuna fishery.

47.9% of respondents have already invested more than £10,000, and 19.2% have invested more than £50,000. One respondent reported commissioning a dedicated boat build in excess of £175,000 specifically for recreational tuna fishing. These are not speculative or modest commitments — they are the kind of capital expenditure that reflects deep confidence in the fishery's long-term value.

What Has Been Invested In

Respondents reported investment across the following categories (multiple selections permitted):

- Rods — 93.3% of respondents

- Reels — 92.0%

- Boat upgrades — 69.3%

- Safety equipment — 61.3%

- Marine electronics — 58.7%

- Travel and accommodation — 38.7%

The picture this creates is of a community that has not just bought a rod and reel. The majority have invested in vessels, safety systems and navigation electronics — the kind of infrastructure that underpins serious offshore fishing capability.

Participation: Well Beyond Occasional

The survey asked respondents how many tuna fishing days per year they would realistically expect to participate in, given current or anticipated access.

95.9% of respondents expect to fish for six days or more per year, and nearly half — 48.6% — expect to participate in more than 20 days annually. This profile is not consistent with casual or occasional interest. It reflects a community of dedicated offshore anglers for whom tuna fishing is a central part of their season.

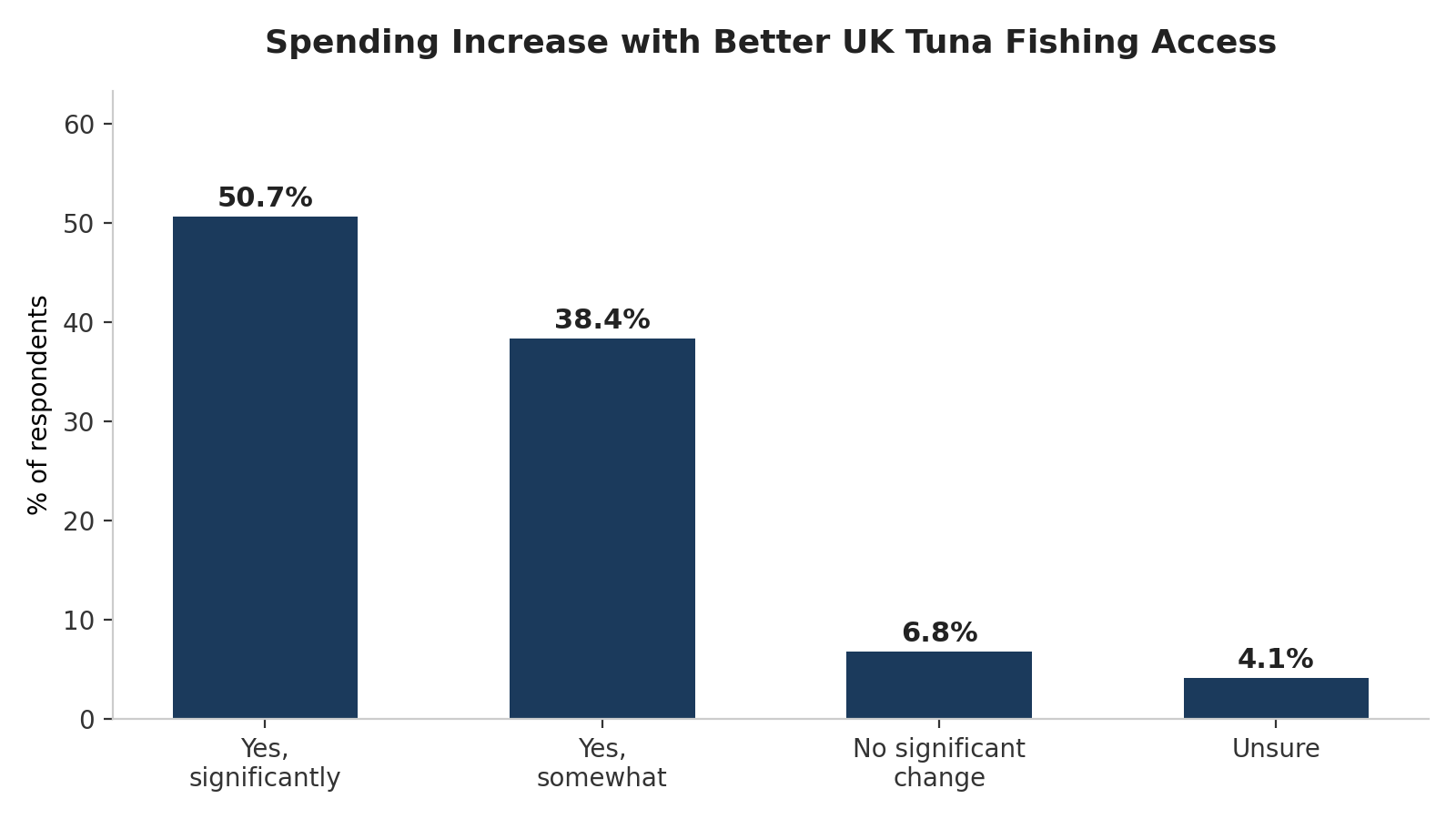

Future Spending: Significant Potential

The survey asked whether respondents would increase their spending if access to the fishery became greater or more regular. The results were clear.

89.0% said yes — either significantly (50.7%) or somewhat (38.4%). 6.8% indicated no significant change, and 4.1% were unsure.

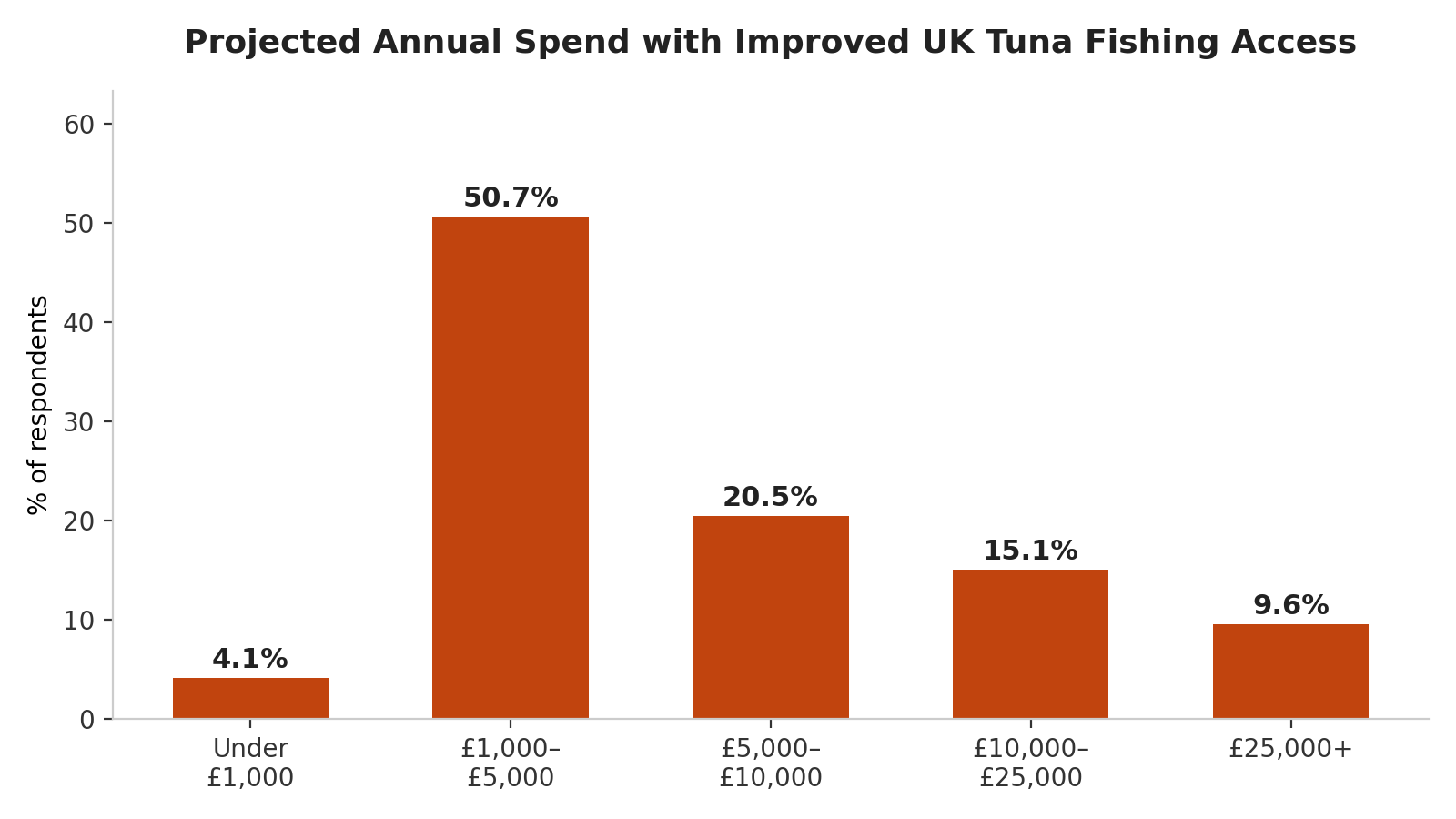

When asked to estimate the additional annual spending that improved access would generate, respondents reported:

24.7% of respondents projected additional spending of more than £10,000 per year with improved access. Across 75 respondents alone, the aggregate additional spending projected runs to a very substantial figure — and this survey represents only a fraction of the total UK recreational tuna community.

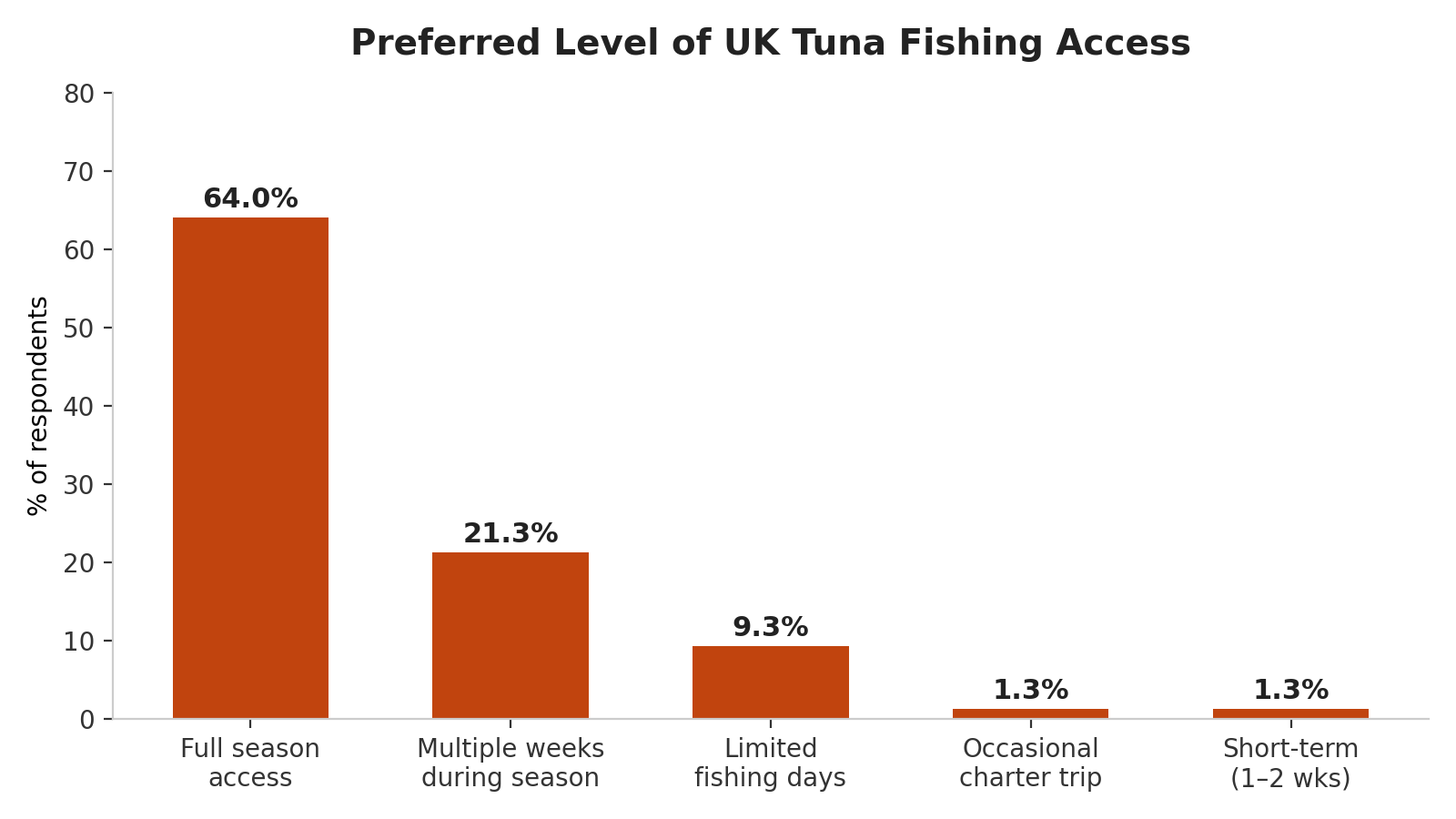

Preferred Access Level

The survey also asked what level of access would best suit respondents' operational needs.

64.0% identified full season access as their preferred arrangement, with a further 21.3% seeking multiple weeks. Several respondents noted in comments that flexible access — rather than fixed advance dates — is especially important given the weather dependency and logistical demands of offshore fishing.

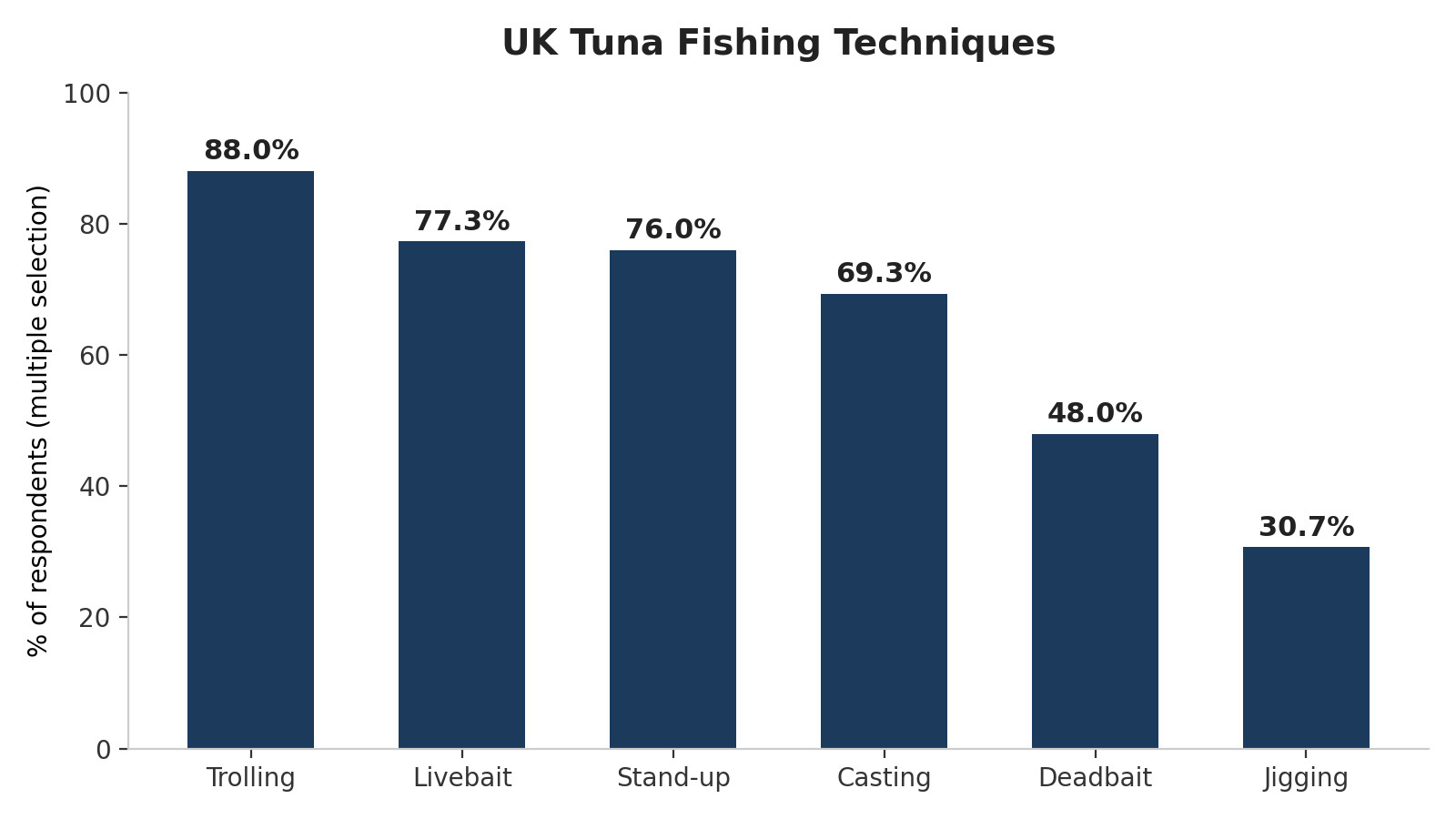

Techniques: A Multi-Method Fishery

The survey documented the range of techniques participants use or plan to use. Results show this is not a fishery defined by a single style of fishing.

Trolling is the most widely adopted method, used or intended by 88.0% of respondents. Surface casting and stand-up fishing — the methods most visible in UK tuna media — are both widely used, but the data confirms that the UK recreational fishery has diversified significantly. The majority of respondents use or intend to use multiple techniques depending on conditions.

What Respondents Said

Alongside the quantitative data, the survey collected open-ended comments from participants. A number of themes emerged consistently.

Experience and offshore capability. Many respondents described extensive offshore fishing backgrounds, with references to blue water game fishing experience, vessel qualifications and multi-season bluefin participation. The recreational tuna community is not a newcomer community.

Investment made ahead of access. A recurring theme was the willingness to commit significant capital — vessels, electronics, specialist tackle — in anticipation of the fishery, even without guaranteed future access. This reflects strong long-term confidence in the fishery's development.

Flexibility and weather dependency. Respondents repeatedly noted that offshore fishing is subject to weather windows, work commitments and sea conditions that make fixed-date participation impractical. Flexible access arrangements were widely described as an operational necessity rather than a preference.

Geographic spread of bluefin encounters. Several respondents noted sightings and encounters in waters not traditionally associated with UK tuna fishing, including offshore areas of Scotland, the East Coast and Wales. This aligns with wider observations of expanding bluefin distribution in north-east Atlantic waters.

Summary: Key Data Points

For quick reference, the headline findings from the 2026 UKTuna survey:

- 75 respondents from across the UK

- 97.3% have already made investments connected to the fishery

- 47.9% have invested more than £10,000; 19.2% more than £50,000

- 95.9% expect to fish six or more days per year

- 48.6% expect to fish more than 20 days per year

- 89.0% would increase spending with improved or more reliable access

- 24.7% project additional annual spending above £10,000 with better access

- 58.1% are based outside the South West of England

- 64.0% prefer full season access

- 88.0% use or plan to use trolling; 76.0% stand-up fishing; 69.3% casting

About This Survey

The UKTuna survey was conducted independently to document participation, investment, and demand within the UK recreational bluefin tuna sector. It is designed as a longitudinal resource — a baseline against which the development of the fishery can be tracked over time.

This survey closed in July 2026 with 75 responses. UKTuna thanks everyone who took part — the results form the baseline dataset for tracking the fishery's development going forward.

Report compiled by UKTuna. Data current as of July 2026. All figures derived from survey responses. For queries contact UKTuna via uktuna.com.

Read more